Insurance Generics: What You Need to Know About Low-Cost Medications and Coverage

When you hear insurance generics, brand-name drugs that are legally identical in active ingredients but sold at a fraction of the cost after patent expiration. Also known as generic medications, they’re the backbone of affordable healthcare for millions of people on fixed incomes, high-deductible plans, or no insurance at all. Most insurance plans push insurance generics because they cut costs without cutting effectiveness. The FDA requires them to work the same as the brand-name version—same dose, same strength, same route of administration. If your doctor prescribes Lipitor, your pharmacy will likely give you atorvastatin unless you specifically ask otherwise. And if you’re on Medicare Part D or a private plan, you’ll pay far less for the generic.

But not all generics are treated the same. Some insurance plans have tiered formularies: Tier 1 is usually the cheapest generic, Tier 2 a slightly more expensive one, and Tier 3 or 4 might be brand-name or specialty drugs. If your plan doesn’t cover a generic you need, you can often appeal or ask your doctor to switch to a preferred alternative. It’s also worth checking if your pharmacy offers discount programs—some chain pharmacies sell common generics like metformin or lisinopril for under $5 a month, even without insurance. And while generics are safe, don’t assume all are equal. Some people report slight differences in how they feel on different brands of the same generic, especially with drugs like levothyroxine or seizure medications. If you notice a change after switching, talk to your pharmacist or doctor.

Prescription savings, the reduction in out-of-pocket costs achieved by choosing generic drugs over brand-name versions. Also known as drug cost reduction, it’s not just about the pill price—it’s about staying on your meds long-term without skipping doses because you can’t afford them. Studies show people are far more likely to take their medicine regularly when it’s cheap. That’s why medication costs, the total amount paid for drugs over time, including copays, deductibles, and out-of-pocket expenses. Also known as drug spending, it’s one of the biggest reasons people end up back in the hospital. Skipping pills because they’re too expensive leads to worse outcomes—higher blood pressure, uncontrolled diabetes, more ER visits. Insurance generics fix that by making treatment sustainable.

And then there’s insurance coverage, the portion of drug costs paid by your health plan, which varies by plan type, tier, and pharmacy network. Also known as drug benefits, it’s not always obvious what’s covered until you’re at the counter. Some plans require prior authorization for certain generics. Others only cover generics from specific manufacturers. A few even have step therapy—you have to try the cheapest generic first before they’ll pay for anything else. Know your plan’s rules. Ask your pharmacist to check your coverage before you leave the counter. And if you’re on multiple meds, ask for a medication review—many pharmacies offer this for free.

What you’ll find below are real stories and practical guides on how to get the most out of your insurance generics. From how to spot a good generic pharmacy to what to do when your plan denies coverage, these posts give you the tools to save money without sacrificing health. Whether you’re managing diabetes with metformin, controlling blood pressure with lisinopril, or treating anxiety with sertraline, you’re not alone—and you don’t have to pay more than you need to.

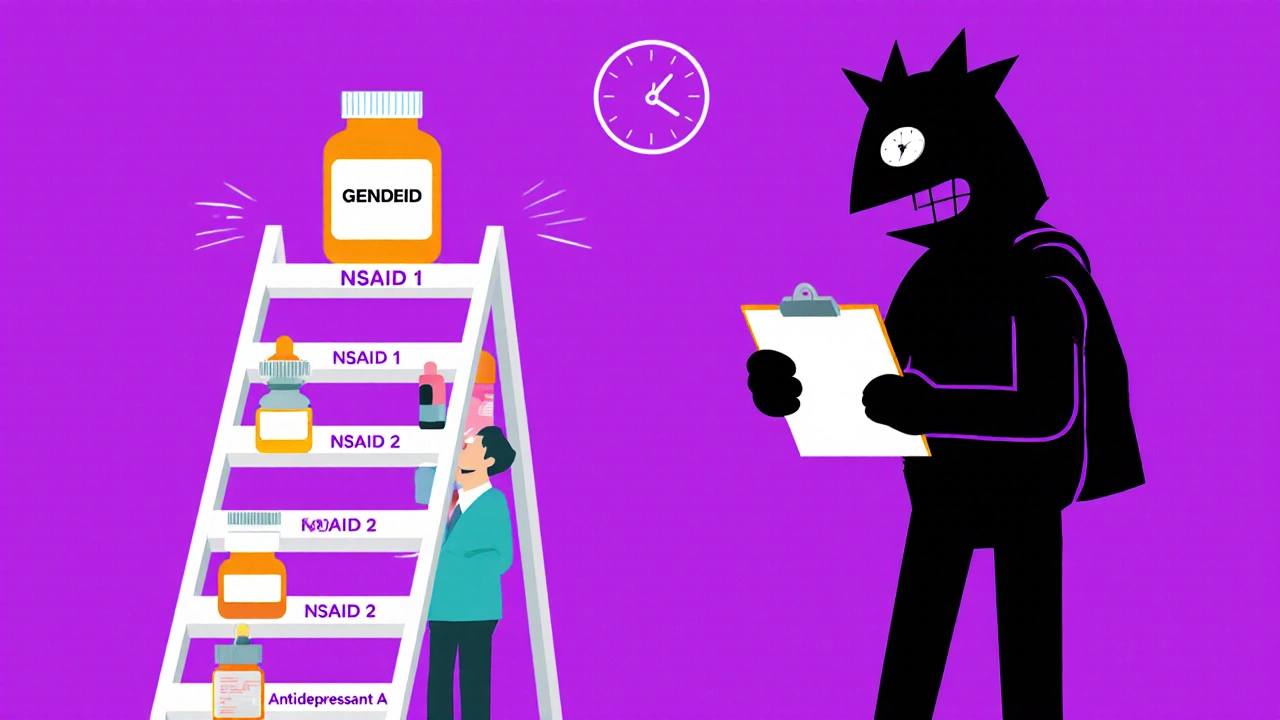

Step Therapy Rules: What You Need to Know About Insurance Requirements to Try Generics First

Step therapy forces patients to try cheaper generics before insurers cover prescribed medications. Learn how it works, when it puts your health at risk, and how to fight denials with proven strategies.

Read More